Recently, we hosted a webinar to discuss issues impacting company general meetings and year-end reporting in 2021, and how companies might best account for them in their planning. The discussion included aspects such as the use of technology to support governance efforts, considerations for their annual reporting in relation to s.172 disclosures, and practical considerations for an AGM in a post 2020-COVID environment with the evident increased focus on stakeholder engagement.

In this article we are going to explore some of these aspects in a bit more detail and provide some signposts to useful resources and assistance available to you from the Computershare team.

Maturing your governance framework in a digital age

We see more and more clients wanting to drive innovation regarding technology and a greater awareness about what is possible with technology today and in the future. This is evident from the GEMS Lead and Learn forums, which we host. These forums provide the opportunity for company secretaries and governance professionals to exchange insights and views on how technology is used and sharing thoughts and ideas about how to work smarter, save time and create value. Our technology white paper, "Maturing Your Governance Framework in a Digital Age", was a result of these forums, the insight we received from the attendees, as well as what we hear from our clients generally.

The key themes resulting from our forums, which often resonate with other clients when we share this information, were that they are looking for technology which can:

- achieve a "single version of the truth" (i.e. a reliable single source of data which can be used by all parts of the business)

- help clients navigate the ever-changing governance and compliance requirements from across the globe

- use data intelligently through analytics and data visualisation

- save time by managing workflows more efficiently

Technology and annual reporting

Driving innovation, understanding what your legal entity management technology can do for you and maximising that usage will help you in countless ways, including with your annual reporting.

It can help by:

Demonstrating compliance

An appropriate enterprise wide platform with the ability to provide a single source of truth will be able to help you accurately report on your compliance with statutory and regulatory requirements.

Reporting on legal entity data and subsidiaries

Housing all your data on a trusted central repository, with complete and accurate information, which is regularly validated, will bring you comfort when reporting on the accuracy of your legal entity data or your subsidiaries.

Management of risk

Implementing a system which has the right data analytics and AI so that you can easily extract and evaluate data, as well as present it appropriately, together with building in the appropriate checks and balances will be of great benefit when demonstrating the effective management of risk within your business.

If you would like to attend our GEMS Lead and Learn forums, or would like to discuss any support regarding the above, please feel free to contact Georgina Milis, Computershare Governance Solutions Director.

s.172 Statements – first year review

As you'll know back in 2018 the Companies (Miscellaneous) Reporting Regulations introduced the requirement for a statement to be included within the strategic report delivering against the objectives shown in the graphic below. This requirement was supported by the updated Corporate Governance Code.

The statements should achieve the following aspects:

1

Demonstrate the directors have discharged their duties

2

The Strategic Report must have a s172 statement heading and be clearly identifiable (with cross-referencing)

3

Report on directors with regard to the 6 factors within the Act

4

Be meaningful and informative for shareholders, focusing on matters of strategic importance for the Company

5

Detail how the Board obtains comfort that stakeholder relationships are managed effectively

6

Describe how sufficient visibility of stakeholder engagement activities is given in the Boardroom to inform decision making and delivery of strategy

7

Be made available on the Company’s website

8

Report on the Company’s broader set of stakeholders and their interests

From a review of the statements released so far in 2020 (focusing on the work of Boards in 2019), it’s clear that three general approaches have been taken to reporting, as described below. Having said that, there aren’t limitations that require you to follow a single approach and it’s important to report in a way that conveys an authentic and balanced view of the work of the board of the company in question.

Stakeholder Led

Statements built around stakeholders and how decisions impacted each group

Cross-referenced to content used to tell the Company’s story

Ensure it is linked to the long-term success of the Company

Based on 6 Factors

Reporting is structured to align with how the matters are set out in s172(1) (a) – (f) of the Companies Act, explaining the actions of the company in relation to each subsection, often cross-refencing to information elsewhere

Ensure outcomes are included

Decision Focused Statements

Details the stakeholder considerations in relation to principal Board decisions during the period

Typically, best incorporated with another approach

Nicholas Pervin, Computershare Governance Solutions Manager advises that in order to get best out of your statements, companies should ensure that they don't duplicate information, while making sure readers of the report can easily identify where to find relevant information.

His advice is that simply relying on a company's framework of policies and processes is not enough and companies need to consider all material issues that are likely to impact the long-term success of the company.

The s.172 statement is the opportunity to tell a balanced story of the company and reflect on the board's oversight and effectiveness. Where possible, consider the use of case studies to provide colour and depth to the story you are trying to tell.

Remember to start early and use evidence you've collected throughout the year (e.g. board minutes, investor roadshows, etc.) when writing your statements. Consider how the statements reflect the widest possible view of your stakeholders. Don't forget you'll need to be clear on the impact of COVID, Brexit and other ESG matters in your 2021 reports .

Issuers with a premium listing on the London Stock Exchange should also remember to be mindful that they too may be subject to the reporting requirements of the updated Corporate Governance Code. As such, they will need to provide a report on how key stakeholder interests have been considered in board discussions or explain why they are not complying with the Corporate Governance Code, despite the s.172 disclosures only relating to UK incorporated companies.

If you need assistance in the planning, preparation or drafting of your statements, Nicholas and his colleagues are available, to discuss annual reporting requirements, ensuring your own company knowledge is paired with a broader market and best practice perspective.

Key reporting considerations

Beyond s.172 disclosures, it is important that governance professionals don't forget some other key considerations for the annual report. Based on our experience and reviews of the market, here are some of the things that we think will be of most importance as you draft your 2021 reports.

Remuneration Disclosures

Impact of Covid-19

Executive Pension alignment

Link to ESG metrics

Post-Employment Shareholdings

Risk Reporting

Impact of Covid-19

Impact of Brexit

Reflect on the impact of individual risks

Covid-19

Disaster Recovery Implementation

Preparedness for future disaster recovery

Short and long-term effects of the pandemic and the impact on strategy

Brexit

Preparedness for no-deal (or possible late deal)

Impact on the Company and its strategy

Any impact on risk management

Audit Quality

Clearly articulate why the Company is satisfied with the Audit quality

Why the Auditor is recommended for (re)appointment

How the Auditor maintained independence and controls

Diversity

Parker Review – Boards required to increase ethnic diversity

Not ‘one and done’

Explain how you expect to be compliant, if not already

Consideration given to wider diversity factors

Future of Corporate Reporting

FRC discussion paper

Suggests a series of interconnected reports

FRC seeking comments by 5 February 2021

Taskforce for Climate Related Financial Disclosures (“TCFD”)

Compliance required by 2022 with the Taskforce for Climate related Financial Disclosure principles

Early planning for your AGM

During the webinar we considered the impact 2020 would have on holding an AGM in 2021. While the market for the latter part of the 2020 season (and the first three months of 2021) is able to rely on the emergency provisions found within the UK's Corporate Governance & Insolvency Act, current expectation is that these accommodations will not be available beyond March 2021.

The legislation only permits the UK government to extend the provisions in three-month intervals and not beyond 5 April 2021. The current extension now runs out on 30 March 2021, which while great news for those issuers planning meetings in the first quarter, provides no certainty for issuers planning meetings thereafter, including during the height of the 2021 season in April and May.

However, for those clients incorporated elsewhere in Europe, the story may be somewhat different.

Irish Companies

The Companies (Miscellaneous Provisions) (Covid-19) Act 2020 is similar in nature to the UK’s temporary legislation in granting issuers the ability to hold virtual and hybrid meetings. One key difference is that at the time of writing, the emergency provisions only extend until December 2020. An extension beyond that date is expected but has yet to be announced. Therefore, Irish companies, like those in the UK, need to mindful of early planning and contingency considerations.

Other European Companies

Throughout the rest of Europe, member states have taken or are taking different approaches to the 2021 AGM season. For instance, temporary legislation in Germany provides issuer certainty by allowing virtual or hybrid meetings until the end of December 2021. In Scandinavia, legislation already typically permits such meetings to take place. Spain have announced that their temporary legislation has been extended to give clarity into 2021. In the Netherlands and France, extensions are restricted based on the drafted legislation, with French companies tending towards closed door meetings as seen in the UK during 2020. The general trend appears to be towards European countries favouring facilitating arrangements which improve shareholder engagement and facilitate more interactive AGM solutions and remote participation. While webcasting or audio conferencing are nice to have, member states are moving towards video conferencing being a minimum standard. Some companies are even considering holding events prior to the closure of the proxy voting periods so that members can engage with the board before casting their votes. This is something that is supported by the recent FRC paper, and we understand is a suggestion being discussed by several large issuers in the UK.

Recent discussions with the Financial Reporting Council indicate a desire to consider practical solutions to the challenge associated with shareholder participation once the emergency legislation in the UK falls away after 30 March 2021. This aligns with the announced work of the FRC on establishing a working group detailed within their Review of the 2020 season.

The report also identified the benefits of introducing technology both to aid in contingency planning and improving shareholder engagement where restrictions are in place on social gatherings.

When planning for 2021 it is incumbent on Issuers to identify what the best solution will be for your board and your stakeholders. For those companies who feel a fully virtual meeting, or even a hybrid meeting, is not appropriate given their circumstances, active consideration should be given to a webcast, which is a strong alternative to a simple audiocast.

Many shareholder groups and proxy advisers are growing in their support of technology and are keen on the introduction of digital voting solutions so long as shareholders, proxies and corporate representatives clearly understand how to use the options available to them. Care should be taken to ensure that whatever format of meeting you decide is most appropriate for your circumstances, there is no real or apparent attempt to discourage shareholder engagement or limit the ability of stakeholders to hold the company to account.

The means by which companies facilitate shareholder/stakeholder engagement is going to be in focus in 2021 regardless of where you are incorporated. We've seen shareholder groups complain about not being able to properly hold the board to account during 2020. So, consider if separate engagement sessions or events are appropriate. Or, consider if the solution discussed by the FRC may work for you, whereby the company might consider holding an engagement session before the proxy voting of the meeting closes, thus ensuring that Issuers can still complete the formal part of the business having had those more traditional Q&A with their shareholders.

The best practice for 2021 is:

Early Planning

Consider all options and have contingencies

Engage with experts (including us)

Check your articles

Prior to the Meeting

Clearly communicate with shareholders

Adopt dedicated methods for shareholders to raise questions

Provide a dedicated website location for relevant information

Clear instructions on using any digital solutions adopted

Questions & Voting

Questions in real-time

Release a full transcript of Q&As

Give enough time to allow questions to be submitted

Utilise multiple voting solutions

Consider electronic proxy reminders

Be clear on how questions may be grouped or moderated

What clients have told us

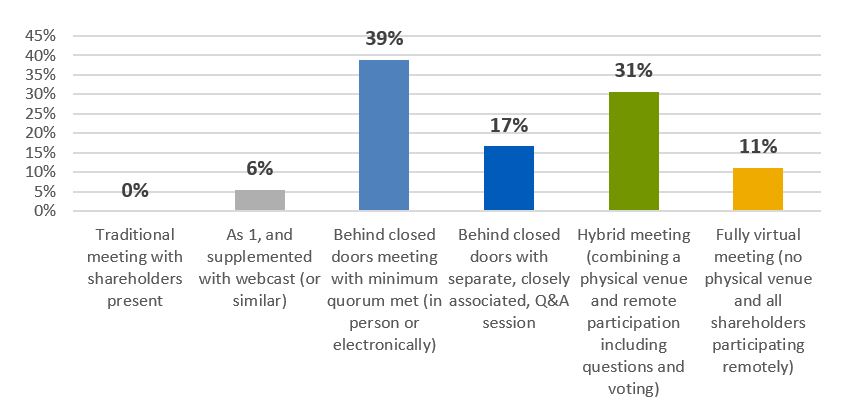

We've been asking clients for their views on the likely format of their 2021 company general meeting. Here's what they told us.

First, we asked for their view on the likely format of their meeting should the current restrictions on social gatherings/meetings remain broadly the same as they are now. Most respondents (39%) felt that their first choice would be to keep a closed-door meeting. As referenced above, this approach is likely to come in for some criticism from the proxy advisers, shareholder groups and potentially also the FRC and government.

However, 31% of respondents felt they would be exploring a hybrid meeting solution, combining a physical venue with remote participation options. The third most favoured approach was a closed-door meeting with a separate Q&A session.

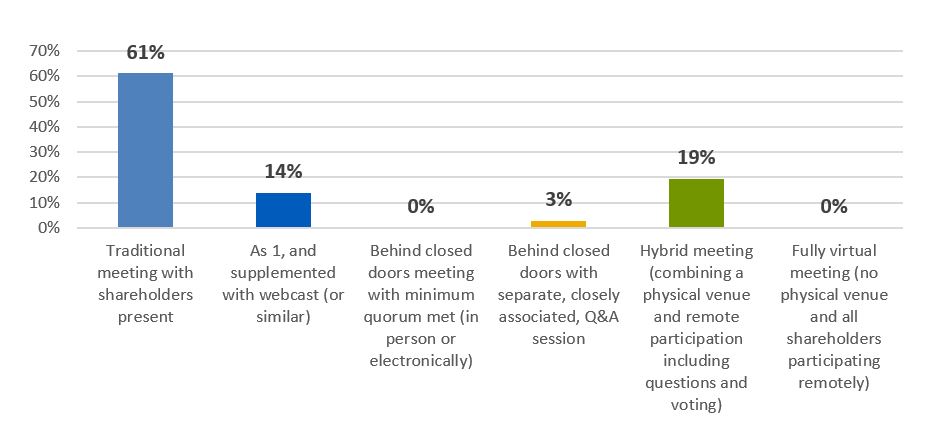

Our survey then asked respondents to suggest what their preferred meeting format would be if the current restrictions on social gatherings were withdrawn and more traditional meetings can be held. Most respondents (61%) suggested that their preferred option would be a return to pre-pandemic style meetings, with a physical venue. This too is likely to attract some criticism given the newfound acceptance of both the technology to facilitate remote participation by shareholders and the potential benefits that could be derived by making meetings more open to geographically dispersed shareholders and those unable to attend a chosen venue at a specific date/time. Again, the second most common choice for respondents (19%) was to consider the introduction of a hybrid solution.

At Computershare we've witnessed a significant shift taking place in the US and many other global markets, with rapid adoption of technology designed to facilitate remote participation. However, the UK and Irish markets have been slow to follow suit, and the absence of legislation to ensure fully virtual meetings are beyond challenge, is a barrier for some. However, the impact of COVID-19 on the speed of change has been immense, and it feels like a matter of time before remote meeting participation is adopted as best practice.

A third question in our survey asked respondents to rank what might influence their decision on how they held their 2021 AGM. Respondents equally felt that confidence in technology being used and the desire to provide shareholders with a way to participate were the most important factors, quickly followed by difficulties with having board members attend and the cost of available technology solutions.

Concluding remarks

2021 is sure to be another challenging year both in terms of drafting reports, disclosures and statements that provide a true, fair and accurate reflection of their achievements and challenges; and in terms of engaging with shareholders and stakeholders. It's worth making sure you are planning early and factoring in what may happen if restrictions aren't lifted or governmental clarity is not quick to arrive.

Computershare are here to assist, whether it is with helping you establish an effective governance framework, crafting your disclosures or planning and executing your AGM.